At Contractors Liability, we offer tailored policies for your roofing business in Texas, and you can include Commercial Auto, General Liability, Inland Marine, Workers’ Compensation, and much more.

If you’re a roofing contractor in Texas, you know that your work involves a certain degree of risk. From working at heights to handling heavy equipment, accidents can happen on the job, and they can be costly.

That’s why having roofing insurance Texas contractors can rely on is so important for roofers. Insurance not only protects you and your business from financial losses but can also help you attract new clients who value safety and responsibility. Let’s explore the reasons why insurance is a must-have for roofers in Texas.

The cost of roofing contractor insurance in Texas depends on your annual revenue, crew size, roof types worked on, claims history, and the state's weather and licensing factors. The estimates below provide a general idea of what roofing contractors can expect to pay for general liability insurance.

| Annual Revenue | Estimated Annual Premium | Estimated Monthly Cost |

|---|---|---|

| $50,000 | From $3,100 | $258/mo |

| $100,000 | From $3,100 | $258/mo |

| $150,000 | From $3,100 | $258/mo |

| $250,000 | From $4,100 | $342/mo |

| $500,000 | From $6,700 | $558/mo |

| $750,000 | From $10,050 | $838/mo |

| $1,000,000 | From $11,400 | $950/mo |

Disclaimer: These pricing examples are estimates for informational purposes only. Actual premiums vary based on underwriting guidelines and individual business factors.

General liability insurance is an essential policy that protects businesses from third-party claims related to property damage or injury. Although not mandatory in Texas, this coverage pays for legal costs and medical bills associated with such incidents. This insurance is particularly important for the construction and roofing industries, where businesses face more risks than other types of contractors. Without adequate coverage, a business may suffer significant financial losses due to claims.

Having the right roofing insurance Texas businesses need can help protect both your company and your reputation. Clients are often more willing to work with businesses that have the proper coverage, as it demonstrates that the business takes safety seriously. By having general liability insurance coverage, roofing contractors can focus on providing quality services without worrying about the financial consequences of potential accidents or property damage claims.

Texas General Liability Insurance Coverage Includes:

There are several factors that determine the final price of general liability insurance, but the most significant factors are the state and the type of work being performed. For roofers in Texas, the cost is typically around 2% to 3% of their annual revenue. Other factors that may affect the price include the number of employees, claim history, and the chosen deductible and coverage limits.

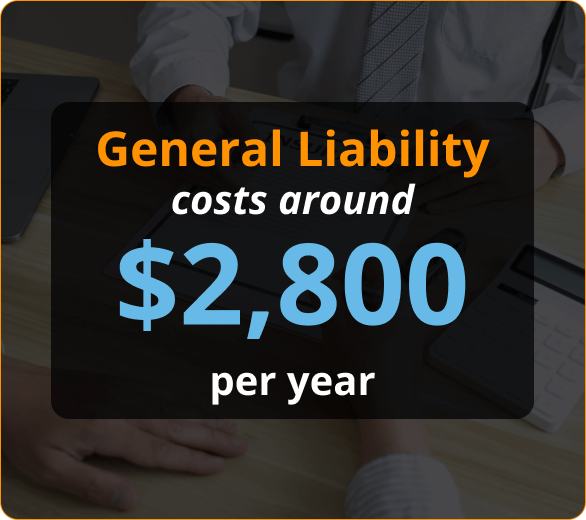

We highly recommend you have a minimum coverage of $1 million with a $2 million aggregate. You can get more coverage, but this is the minimum we suggest. General liability costs around $2,800 per year.

Before obtaining General Liability Insurance, it is important to consider that there are certain occasions where coverage may not be offered due to exclusions. The following exclusions should be taken into account:

Open roof exclusions

In Texas, private employers are typically not required to have workers’ compensation, but strict requirements must be followed if coverage is not in place. It is advisable to have a workers’ compensation insurance policy if there are employees or uninsured subcontractors, as this type of policy covers medical bills and expenses related to work-related injuries.

The premium for this policy is based on the payroll, the work performed by employees, and the employer’s safety record. If a roofing contractor has a contract with a large general contractor, has insured subcontractors, or has no employees, an “If Any” or Ghost policy may be used.

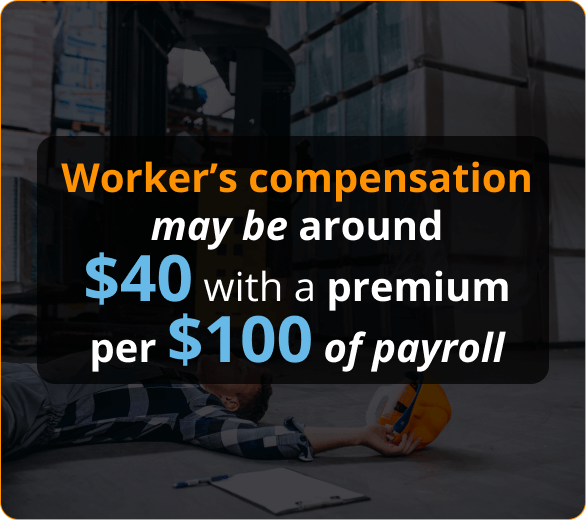

It is important to keep the certificate of insurance for insured subcontractors to avoid any liability issues during policy audits. The cost of the policy is determined by factors such as the payroll, the type of work performed, location, years in business, and safety record. For roofing contractors, the premium per $100 of payroll may be around $40.

If you use vehicles for commercial purposes such as transporting equipment or materials to job sites, Commercial Auto Insurance can provide coverage in case of an accident. This type of insurance typically offers better coverage and benefits compared to Personal Auto Insurance, and the cost is often only slightly higher.

Additionally, the cost of Commercial Auto Insurance may be tax-deductible, making it a more affordable option.

This type of insurance covers:

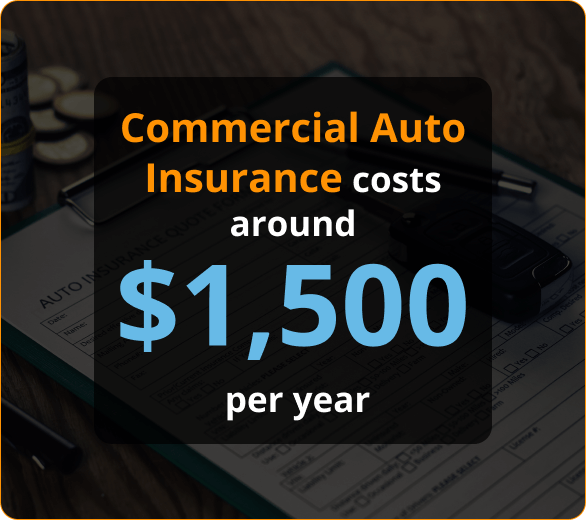

The cost of the policy is determined based on factors such as the number and type of vehicles, the number of employees, the amount of revenue, the location of the business, and the driving records of the insured. On average, Commercial Auto Insurance costs around $1,500 per year.

Inland Marine insurance is essential for roofers as it provides comprehensive coverage for their specialized tools and equipment used during transportation and on job sites. This insurance safeguards a wide range of crucial items, including:

Roofing Tools: Nail guns, roofing hammers, shingle cutters, ladders, safety harnesses, and scaffolding are protected against theft, damage, or loss, ensuring that roofers have the necessary equipment to carry out their work efficiently.

Materials and Supplies: Inland Marine insurance covers roofing materials such as shingles, tiles, sealants, adhesives, and insulation, protecting them from theft, vandalism, or unforeseen accidents that may occur during transportation or while stored on-site.

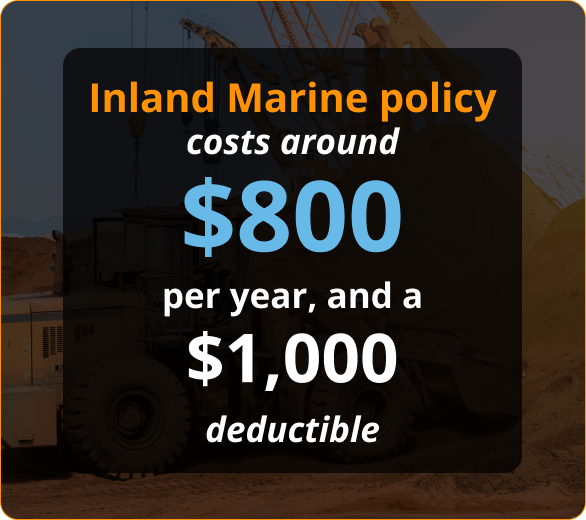

Your equipment is crucial to your job, and Inland Marine insurance helps safeguard it from theft or damage. The cost of the policy varies depending on factors such as the value of the equipment being covered, the state, the claim, and the credit history of the business. The minimum premium for this policy is $500, with most policies costing around $800 per year, and a $1,000 deductible. This typically provides coverage of $100,000 for the insured property.

This specialized type of insurance covers construction in progress. Builder’s risk insurance in Texas is an essential type of coverage that ensures a building under construction is protected from property damage caused by Lightning, explosion, fire, hail, vandalism, theft, and acts of God (major weather events, etc.).

Builder’s risk isn’t just for the builder. Anyone with a financial stake in the construction project should be included in the policy. This includes the property owner, lender, architect, general contractor and subcontractors. Aside from property damage, this Texas builder’s risk insurance covers other expenses outside of the construction itself.

Some of these costs include:

The minimum premium for this policy is $500, with most policies costing around $800 per year, and a $1,000 deductible. This typically provides coverage of $100,000 for the insured property.

Commercial Umbrella Insurance in Texas is an additional layer of protection for paying claims when the amount of the claim exceeds the current limits of other liability policies. If you don’t have commercial umbrella insurance in Texas, any amount that your standard liability policies don’t cover would have to be paid out of pocket. This can create a financial liability that can ruin a business.

Some of the things that may not be covered by standard policies include: Medical bills, including current or future treatment, Legal expenses or the cost of pursuing coverage, damage to public property or other people’s property that may be damaged.

Texas commercial umbrella insurance acts as an extension of other policies, and it works to absorb additional financial liability associated with insurance claims against your business or employees.

It differs from excess liability insurance, however, because excess liability insurance only extends specific limits on specific policies. Commercial Umbrella Insurance can work across policies of different types.

In Texas, ACORD certificates are designed for holders of specific commercial insurance policies. These certificates are easily portable and are typically only one page in length. They serve as a concise summary of the policy’s key details for third parties.

They may also be referred to as ACORD 25 COI or Certificates of Insurance, as well as Certificates of Liability Insurance. An ACORD certificate issued in Texas will contain crucial policy information, including:

Some of these costs include:

Our experience with roofers allows us to offer the best insurance coverage at the most competitive price.

By purchasing your roofing insurance policies from us, you can save money on your roofing company insurance costs. If you have any questions or would like to speak directly with an agent, please call us at (888) 973-0016 or click here to receive a free quote.

We Have Texas Covered

The following are common questions about Roofers Insurance.

General Liability Insurance in Texas typically requires coverage of $1,000,000 per occurrence and $2,000,000 aggregate. This coverage is typically sufficient for 99% of all General Liability policies sold in Texas.

For Workers’ Compensation Insurance in Texas, coverage of $500,000/$500,000/$500,000 is generally recommended. This coverage protects your workers in the event of a claim where the owner is liable for up to $500,000. In most cases, the owner is not held liable, and coverage for Workers’ Compensation Insurance is unlimited.

When it comes to Commercial Auto Insurance in Texas, you’ll need a Combined Single Limit (CSL) of $1,000,000 to cover both bodily injury and property damage to the other party combined. To protect your Texas vehicle, it’s also recommended to have Comprehensive and Collision coverage. Collision Insurance covers any collision-related damage, while Comprehensive Commercial Auto Insurance covers any damage to your vehicle that isn’t caused by a collision.

Our customers trust us for great customer service and cost-effective coverage.