At Contractors Liability, we provide fast, tailored, and cheap roofing insurance policies! From Commercial Auto to Workers’ Compensation, General Liability, and more! We are your reliable insurance provider, and we answer the phone 24/7 to meet your needs.

Most people know that roofing is one of the riskiest professions in the construction industry. Even a fall from a single-story building can be extremely dangerous for both the worker and other people around the property. Therefore, having the right roofing insurance is essential for the safety of all parties involved in the process.

Contractors Liability provides low-cost insurance for all sorts of roofing contractors. In this article, you will learn what a standard policy of roofing insurance cover, how to calculate the price, and why it is important.

For starters, it’s vital to know that the price of every policy is mainly affected by the following:

The top 3 types of insurance coverage that a roofing contractor in Houston will require are as follows:

Imagine working on a roof and accidentally letting a heavy tool fall on the client’s ceramic floor. How would you handle this?

Roofing Contractors’ Liability Insurance covers third-party bodily injuries and property damage to your client’s property resulting from your job. Additionally, it pays for any medical bills and legal costs incurred if your company is sued due to a covered claim. The average roofing business owner cannot afford to cover these legal costs out of their own pocket because attorney fees can be costly. You, therefore, require a reasonably priced roofers insurance policy.

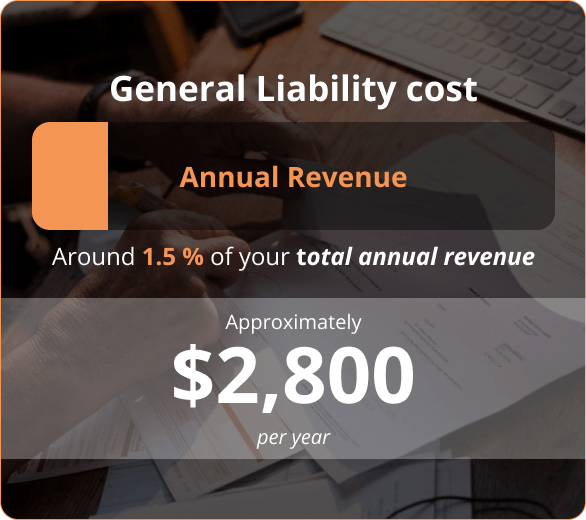

For roofers, General Liability costs around 1.5 percent of your total annual revenue. We advise that the minimum coverage under your liability policy be $1 million, with a potential aggregate of $2 million. The most frequent insurance protection is this, and we encourage you not to settle for anything less. Usually, fewer than $100 can be saved, but the coverage difference is noticeable. These general liability insurance policies typically cost approximately $2,800 per year.

There are also specific exclusions to look out for on your General Liability coverage. These exclusions are critical since they do not provide coverage in certain situations. The four main exclusions are as follows:

This type of policy covers medical expenses and loss of income from work-related employee injuries and diseases. Texas roofing companies are not typically required to carry workers’ compensation insurance, but they should do so. If you don’t have coverage, you must adhere to very rigorous rules. You may find the criteria HERE.

Generally speaking, carrying a reasonable workers’ compensation policy is an excellent practice if you have employees or work with uninsured subcontractors.

Note: You can use an IF ANY POLICY or GHOST POLICY if you don’t have any workers or work solely with insured subcontractors. If you, the contractor, have a contract with a major general contractor, you may typically access these policies. Any subcontractor under these contracts is generally required to show proof of Workers’ Compensation insurance. These policies usually cost roughly $1,500 annually.

You must maintain copies of each insured subcontractor’s Certificate of Insurance since, without them, all payments made would be considered payroll, subjecting your roofing company to a significant premium obligation when your policy gets audited.

Your payroll amount will determine how much your workers’ compensation insurance will cost. The level of risk associated with the employee’s work is calculated (Class Code), and the amount of payroll is multiplied by this risk factor. This amount is typically expressed as the premium paid per $100 of payroll. However, as previously stated, the firm’s location, the time you have been in operation, and your safety record/loss history (Commonly referred to as Experience Modification or EM) are also essential pricing factors.

You will require a business auto policy if you use your vehicles to transport tools and equipment to job sites. Your personal auto coverage does not cover business use. There is a considerable risk that your personal insurance provider would deny the claim if you are in an accident while operating your car for business-related purposes. Despite offering substantially higher levels of coverage and certain other benefits, the cost is not significantly higher than that of your personal vehicle, and since you can deduct this coverage from your taxes, the actual price is practically identical.

As with the other policies, the cost of Commercial Auto Insurance can vary greatly. Along with the general factors that affect most policies, the following are the main factors affecting its price:

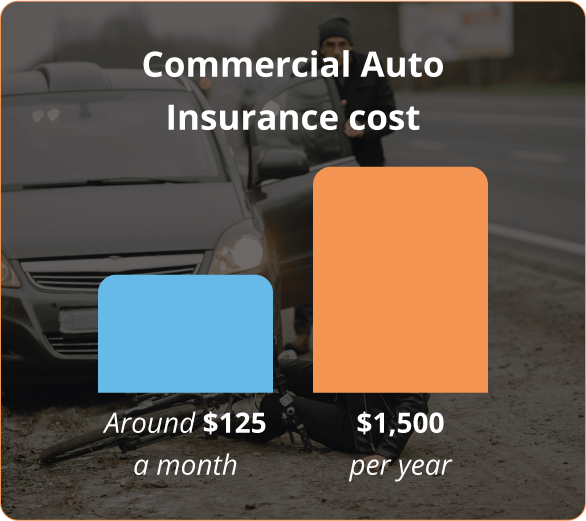

For a policy limit of $1 million, the cost of Commercial Auto Insurance for most businesses is $125 per month or $1,500 per year.

Suppose Bulldozers, skid steers, generators, or other tools are stolen from a project site. In that case, they can be covered by a cheaply priced Inland Marine Coverage. This policy protects your equipment and materials on the job site, in transit, or basically anywhere else.

Most contractors work at various job sites, so having equipment insurance is crucial. Contractors’ enterprises generally obtain Inland Marine to cover their pricey and vital equipment. It’s essential to keep in mind that your tools and equipment are how you sustain yourself. If they were stolen or ruined in a mishap, could you replace them on your own?

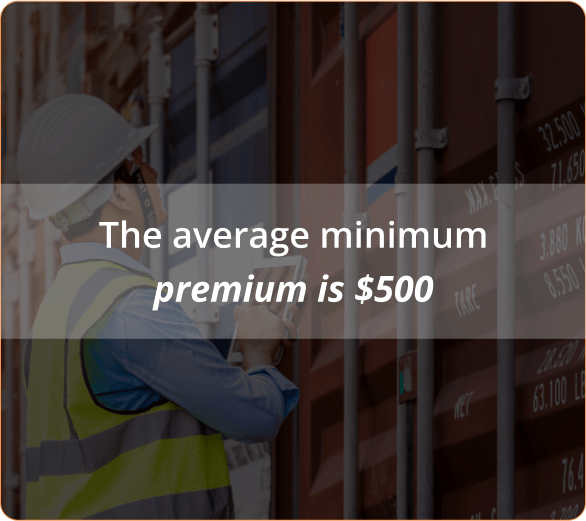

The cost of inland marine depends on many variables, including the cost of the insured equipment, the state, the company’s claim and credit history, and other relevant aspects. For Inland Marine plans, the average minimum premium is $500. However, this insurance usually costs $800 annually to cover $100,000 in protected property with a $1,000 deductible, or $0.80 for every $100 of coverage.

Commercial umbrella insurance is a cornerstone of business protection for roofing contractors in Houston, Texas. Known as excess liability insurance, this coverage expands the limits of your other business insurance policies, providing an essential safety net against enormous losses that could jeopardize your company.

Consider these potential scenarios where Houston commercial umbrella insurance becomes a lifeline:

Additionally, some clients or contracts may require a commercial umbrella policy before any work commences. Discussing your insurance needs with a knowledgeable broker can determine whether an umbrella policy suits your Houston roofing business.

These are the essentials you will need to ensure that your roofing business is adequately insured. If you need to speak with a live agent or have questions, please call us at (888) 973-0016

Contractors Liability is a cost-effective insurance company that can provide you with the best affordable roofers insurance plan with A-Rated Carriers, thanks to their experience with roofers. There is nothing to lose, so give us a call or click right now!

Hesitating because you can’t see your city on our list? We’ve expanded our operations across numerous cities. We’ve got all the Texas cities covered here

Get answers to your most common questions from Contractors Liability

For General Liability Insurance in Houston you need $1,000,000 per occurrence and $2,000,000 aggregate almost 100% of the time. 99% of all General Liability policies we sell in Texas are $1,000,000/$2,000,000.

For Commercial Auto Insurance in Houston you need $1,000,000 CSL meaning $1,000,000 Combined Single Limit for Bodily Injury and Property Damage to the other party combined. To protect your Houston vehicle you need to have Comprehensive and collision coverage. Commercial Auto Collision Insurance in Houston, TX covers any collision and Comprehensive Commercial Auto Insurance covers anything but collision.

For Workers Compensation Insurance in Houston you need $500,000/$500,000/$500,000 in general. This covers your workers in the event of a claim where the owner is liable up to $500,000. In 99% of cases the owner is not liable and coverage for workers compensation is unlimited.

Our customers trust us for great customer service and cost-effective coverage.