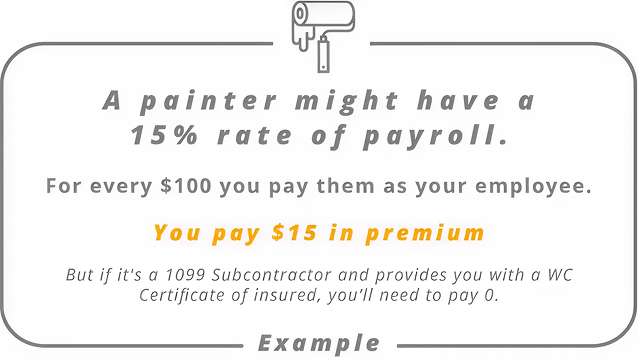

So let’s first think about how Workers Compensation Insurance is billed. Workers compensation is billed by classes of employees and the type of work they do on a percentage basis of payroll. For example, a painter might have a 15% rate of payroll.

This means for every $100 you pay them as your employee (Workers Compensation is meant to cover your employees) you pay $15 in premium. Now if that same painter you pay $100 to is not an employee, but a 1099 subcontractor, and provides you with workers compensation insurance naming your business as additional insured, you would have to pay 0. No problem.