From Florida Workers’ Compensation Insurance to General Liability, Commercial Auto Insurance and More! We Are Your Easy & Stress Free Construction Insurance Provider for Florida Roofers Insurance!

The roofing industry, like the construction industry in general, is known for its potential hazards. Even a small mistake or oversight can have serious consequences, so it is important to consider investing in roofing insurance to protect your business from significant losses and claims. However, choosing the right roofing insurance provider in Florida can be challenging due to the different types of coverage available. To make an informed decision, it’s important to understand the different types of coverage available and determine which ones are best suited to your business’s unique needs.

If you want to get the best coverage now, from the best carriers and at the lowest price, call us at (888) 973-0016 or click for a free quote. We can assist you and answer all your questions 24/7!

The cost of roofing contractor insurance in Florida depends on your annual revenue, crew size, roof types worked on, claims history, and the state's weather and licensing factors. The estimates below provide a general idea of what roofing contractors can expect to pay for general liability insurance.

| Annual Revenue | Estimated Annual Premium | Estimated Monthly Cost |

|---|---|---|

| $50,000 | From $3,106 | $258/mo |

| $100,000 | From $3,111 | $258/mo |

| $150,000 | From $3,116 | $258/mo |

| $250,000 | From $4,250 | $354/mo |

| $500,000 | From $7,000 | $583/mo |

| $750,000 | From $10,500 | $875/mo |

| $1,000,000 | From $12,000 | $1000/mo |

Disclaimer: These pricing examples are estimates for informational purposes only. Actual premiums vary based on underwriting guidelines and individual business factors.

Roofing accidents are common and can occur despite the precautions taken by contractors and business owners. Therefore, general liability insurance is crucial and commonly used by roofing contractors in Florida. It serves as protection against any third-party damages, referring to anyone on or near the job site who is not a contractor working on completing a roofing project. In the event of an accident, the insurance covers costs that would otherwise be paid out of pocket. This includes injuries to bystanders or damage to a customer’s property.

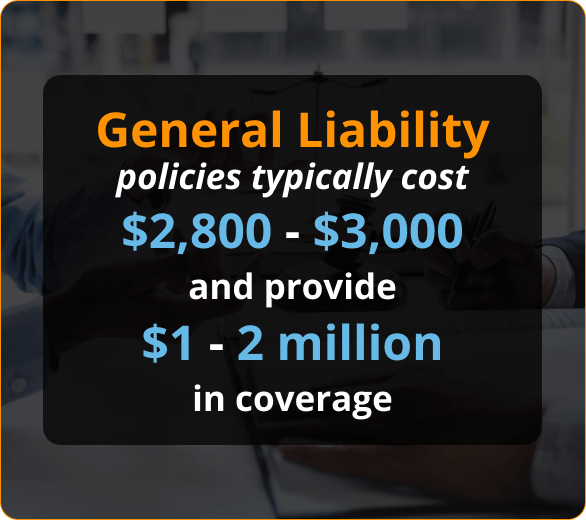

However, general liability claims can be expensive, and the United States is the most lawsuit-prone country in the world. If a roofing company is sued, legal fees can easily run from $20,000 to $100,000 or more. In contrast, a general liability policy typically costs between $2,800 and $3,000 and provides $1 million to $2 million in coverage. In most states, this type of policy is required for a license and is always required for business. Without insurance, a roofing company’s finances can be quickly impacted by a claim, potentially leading to bankruptcy.

General liability insurance is important not only for financial protection but also for protecting the reputation and rights of a roofing company and its employees. It provides protection in the event of customer dissatisfaction with the services or products provided. It also covers claims for libel, slander, mistaken arrest or eviction, and other potentially damaging claims brought by customers. In summary, general liability insurance is essential to the durability and success of a roofing business in Florida.

Workers’ compensation insurance aims to provide financial protection to employees who suffer injuries or illnesses on the job, which could lead to lost wages and high medical expenses. Despite being cautious, accidents can happen to anyone, including employers. This is especially true in the roofing industry, known for its high-risk nature.

As such, having workers’ compensation insurance is essential. In Florida, it is a legal requirement for businesses with more than one employee, but beyond that, it is a smart business practice.

By having this type of insurance, you can avoid personal liability for employee claims and demonstrate that you value and care for your employees. Aside from the legal and ethical reasons to carry workers’ compensation insurance, it is also an affordable option for businesses.

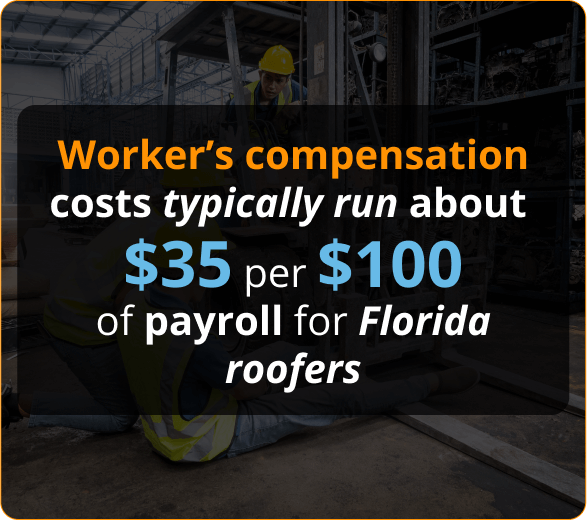

The cost of the insurance typically runs about $35 for every $100 of payroll for roofers in Florida. Moreover, businesses don’t have to assume this cost alone. By increasing the hourly rate by the cost of the insurance (i.e., $35), the hourly rate can be adjusted to cover the cost of the insurance. For instance, if your hourly rate is $100, raising it to $135 would effectively offset the cost of workers’ compensation insurance.

By having this coverage, you not only protect your employees but also bolster your company’s reputation as a fair and caring employer.

Although they may seem similar, commercial auto insurance and personal auto insurance are distinct. Personal auto insurance is likely insufficient to cover vehicles used for income-generating purposes, for which commercial auto insurance policies are specifically designed.

If you run a roofing company in Florida with a fleet of trucks or even just a few vehicles, it’s important to upgrade to commercial auto insurance, as it is a legal requirement in Florida. This insurance provides coverage for physical damage to vehicles and also offers protection for employees who operate your vehicles. However, it’s worth noting that commercial auto insurance does not cover damage or theft of any tools or supplies stored in your vehicles; for that type of coverage, you’ll need to consider inland marine insurance.

One significant advantage of commercial auto insurance is that it’s tax-deductible for your business, which is not the case with personal auto insurance.

Builder’s risk insurance, also referred to as course of construction insurance, provides protection against damages resulting from vandalism, theft, and other incidents while a building project is still under construction. Traditional property insurance, on the other hand, only covers damages to existing buildings or structures and excludes coverage for those that occur during construction or renovation.

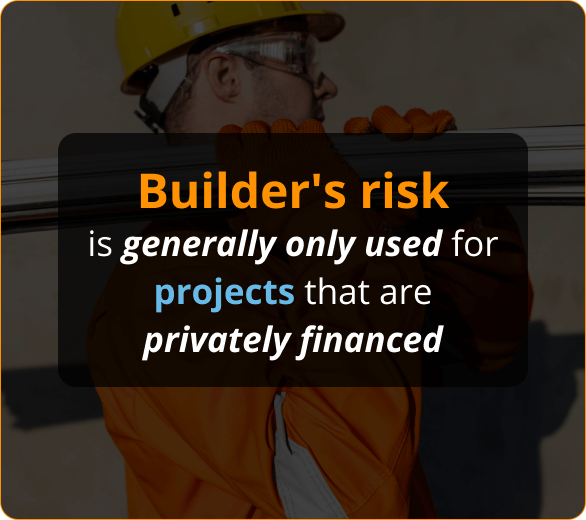

Builder’s risk coverage can be purchased by either the project owner or the general contractor and covers the cost of replacement work and any delays caused by damage. However, this type of insurance is generally only used for privately funded projects, as government-funded projects are usually self-insured. The responsibility for obtaining this type of insurance is typically defined in the contract between the owner and the contractor.

Inland marine insurance is a policy that covers your tools, equipment, and materials while they are in transit between job sites or in storage with a third party. This type of insurance covers replacement costs if your items are lost, stolen, or damaged under covered circumstances.

While it’s a common assumption that tools stored in a vehicle covered by your commercial auto policy are automatically covered, this is not the case. For example, if you transport roofing materials and valuable power tools in the bed of a company pickup truck, they would be covered under your inland marine policy, not your commercial auto policy.

Since the tools and materials needed for roofing jobs in Florida can be quite expensive, you would not want to pay for replacement costs out of your own pocket. For this reason, inland marine insurance can be an important addition to your policy if you frequently transport materials and want to protect them as well as your money.

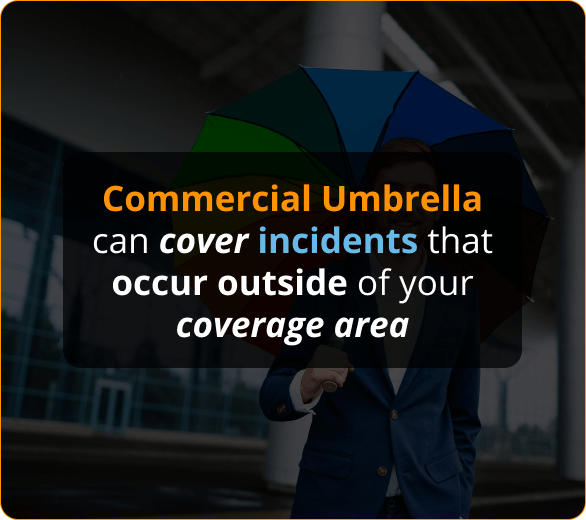

Also known as COI, this is an insurance policy that provides extra coverage for your business in the event that a lawsuit or serious accident exceeds the limits of your General, Auto, or other liability policies. It can even cover incidents that occur outside of your coverage area.

The following are some scenarios in which Commercial Umbrella coverage can protect your company:

SubGuard insurance policy protects general contractors from damages resulting from subcontractor default. This type of insurance helps cover costs incurred when a subcontractor fails to perform their duties.

Subcontractor default insurance can cover the expenses associated with finding a replacement subcontractor and paying them to complete the project, resulting in reduced deductibles and reserve requirements.

To be eligible for coverage under many SDI systems, general contractors must have at least $200 million in subcontractor work. As a result, many small and medium-sized general contractors may not qualify for this type of coverage. For these contractors, more affordable options for protection against subcontractor default include performance bonds and project loss insurance.

We Have Florida Covered

Get answers to your most common questions from Contractors Liability

In Florida, it’s generally required to have general liability insurance with coverage of $1,000,000 per occurrence and $2,000,000 aggregate. Almost always, a policy with these limits of $1,000,000/$2,000,000 is what’s sold, with 99% of the general liability policies we sell in Florida having these limits.

Commercial auto insurance in Florida requires $1,000,000 CSL for bodily injury and property damage to the other party combined. Comprehensive Collision Coverage is necessary to protect your vehicle, with Commercial Auto Collision Insurance covering collisions and Comprehensive Commercial Auto Insurance covering non-collision damages.

Workers’ Compensation insurance in Florida requires a coverage limit of $500,000 per occurrence, per employee for bodily injury by accident and per employee for Disease Policy Limit. While this covers your employees in a claim where the owner is liable for up to $500,000, in most cases the owner is not liable and the workers’ compensation coverage is unlimited.

Our customers trust us for great customer service and cost-effective coverage.