Protect your business from unforeseen risks with comprehensive general liability insurance. Whether you’re a small contractor or managing a larger operation, this coverage shields you from third-party claims related to property damage or bodily injury.

Our tailored solutions ensure that your business stays secure, allowing you to focus on your projects without the stress of potential legal complications.

General Liability Insurance protects contractors from claims made by clients or third parties for damages caused by the contractor or their employees. Despite best efforts to ensure safety, accidents can still occur, making this type of coverage essential.

As a contractor, you work hard to maintain a safe job site and protect your reputation. However, even the most cautious businesses can experience unforeseen incidents. That’s where General Liability Insurance comes in, offering protection for your business, assets, and yourself.

This insurance is often mandatory in most states, ensuring you’re covered for potential liabilities without overpaying. ContractorsLiability.com specializes in providing affordable and reliable General Liability Insurance to keep your business safe.

Protects against claims of injury caused by your business operations or products.

Example: While installing flooring, someone trips over your tools and is injured.

Protects against claims such as libel, slander, or misuse of client images.

Example: Using a client’s home in your marketing materials without permission could lead to a lawsuit.

Covers medical expenses if someone is injured on your business premises.

Example: A client falls and injures themselves while visiting your office.

Covers damage to a client’s or third party’s property.

Example: An employee accidentally damages a client’s vehicle while installing a garage door.

Protects against claims for damage to rented property due to specific incidents.

Example: A propane tank leak from your roofing business causes a fire in a rented building.

Helps protect your business if you’re accused of infringing copyrights or making advertising errors.

Example: You use a brand name in an ad without proper authorization, leading to a claim.

If your business provides advice or professional services, errors or omissions are not covered. For that, you’ll need Errors and Omissions Insurance (also known as Professional Liability Insurance) to protect against claims stemming from advice or recommendations you give.

General Liability Insurance does not cover accidents involving your business vehicles. For that, you’ll need Commercial Auto Insurance to protect against vehicle-related claims.

Most General Liability policies do not cover punitive damages, which are financial penalties in lawsuits intended to punish the defendant.

Damages resulting from intentional actions, such as an employee deliberately damaging property, are not covered by General Liability Insurance.

Faulty workmanship or poor-quality work, often referred to as the “workmanship” or “warranty” exclusion, is not covered. For example, if the paint you applied starts peeling due to improper preparation, this would not be protected by General Liability Insurance.

Is the cheapest General Liability Insurance for contractors always the best?

The cheapest General Liability Insurance for contractors can be perfect for your needs and your wallet. There is no reason to purchase expensive policies or ones that are not suitable to your needs, preferences, and budget.

General Liability Insurance is crucial for protecting your business from costly lawsuits and accidents. It covers legal fees and damages if a third party sues you for property damage or bodily injury, preventing significant financial loss.

Many contracts require this insurance, making it essential for securing projects and maintaining credibility. By having this coverage, you safeguard your business, ensuring peace of mind and allowing you to focus on growth without worrying about unexpected liabilities.

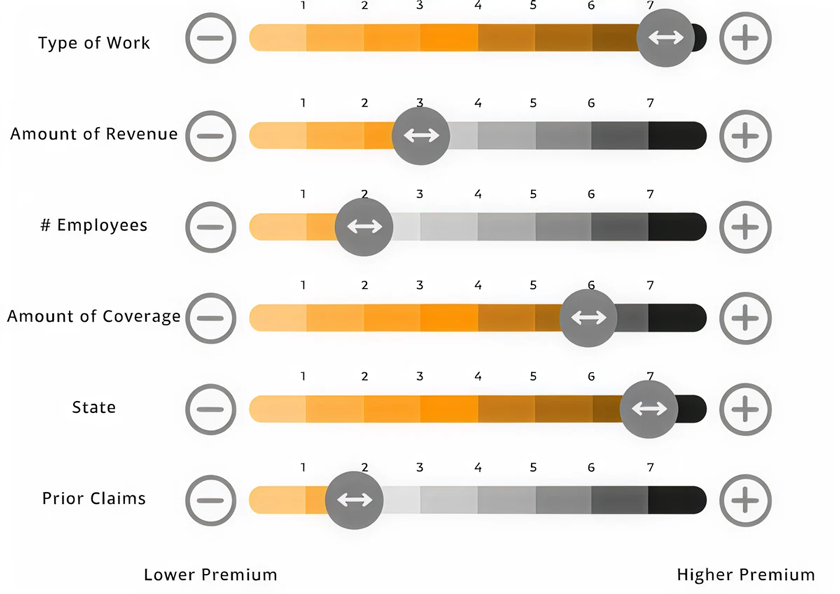

There are common factors that insurance companies use to determine insurance costs. These are:

Once you have purchased a General Contractors General Liability Insurance policy different people or companies may ask you to have them named as additional insured’s on your policy.

The most common requests are from clients who you are doing work for, Cities that you are working in, and landlords to make sure you have coverage as required by any lease you may have. If you will anticipate you will need a number of Certificates of Insurance to be issued you should consider adding a blanket additional insured endorsement to your policy.

This is sometimes included in policies or there maybe an additional charge for this endorsement. The blanket additional insured allows you to add as many clients as you need to your General liability Insurance Policy.

It also offers coverage as long as you have a contractual relationship with a client whether or not a certificate is issued specifically to them. This is especially important if you deal with a large number of certificate request as the chances of making a mistake is great. With the blanket endorsement you are covered.

The most common types of additional insured forms are listed below. They are reference by their ACORD form number. The acronym “ACORD” stands for Association for Cooperative Operations Research and Development. These are standard insurance forms used in the insurance industry:

Along with our customer satisfaction guarantee, we:

In the last few years, insurance carriers are regularly adding the CG 22 94 endorsements to the commercial general liability policy to exclude losses arising out of subcontractor-caused damage to a contractor’s work. The theory behind the CG 22 94 endorsements is that the damage caused by a subcontractor’s work should be the responsibility of the General Contractor as a business loss and not a loss covered by the General Contractors General Liability Insurance Policy.

A number of General Liability carriers that insure home builders and remodelers have added this exclusion. As a result, this exclusion results in a substantial reduction in coverage as compared to prior policies.

There are a number of options you have available to you to get around this exclusion:

It actually is very simple a 1099 is an IRS form that businesses pay non employee compensation to any third party. This by definition makes anyone who receives money that is classified as 1099 income not an employee of the party issuing the 1099. However, just saying someone is a 1099 and not an employee does not make it so.

If to the IRS it walks like a duck and quacks like a duck even if you call it a chicken, they can reclassify the payee 1099 as a W-2 employee. This can result in massive tax liability. So why do contractors try to get away with this? Well, there are 2 main reasons. First if a worker is 1099, the contractor is not responsible for paying employment taxes as they would with a W-2 employee.

The second reason is that for worker’s compensation insurance any money paid on a 1099 is not considered payroll thereby reducing Worker’s Compensation costs. If a contractor is working with Independent Contractors and Subcontractors they must get certificates of insurance from these workers. If they fail to get a certificate they will be treated as uninsured subcontractors on the General Contractors General Liability Insurance Policy.

As a result, any amount paid will be added back to your income for premium purposes. The same goes for Worker’s Compensation Insurance. Also with Worker’s Compensation if someone you 1099 is injured there is a good chance a smart lawyer may make the claim that the injured party was actually an employee. If the court rules they were you could be on the hook for a lot of money.

On the other hand only covers claims made while the policy is in force including any extended reporting period that might be granted. If a claim is made after the policy expires you will not have any coverage even though the claim would have been covered if the policy was in force.

For example A covered claim happens on 10/31/2020. Your General Liability Insurance policy expires 12/31/2020 and you do not renew the policy. As an example, if a claim for the loss on 10/31/2020 is made on 3/1/2021 and you have an Occurrence policy, you will have coverage. This is since the occurrence was in the policy period. If you have a claim made policy you will have no coverage since the claim was made after the policy expired.

Where the event must take place during a set period. This means if a covered claim occurred during the time the policy was in force you will have coverage even if the claim is made after the policy is expired. This is the type of coverage you should have.

No, injuries to your employees are not covered by General Liability Insurance. Employee injuries are handled through Workers’ Compensation Insurance. For example, if an employee falls from a ladder, General Liability won’t cover the medical costs or lost wages.

No, professional mistakes or errors in advice are not covered. For this, you’ll need Errors and Omissions Insurance (Professional Liability Insurance) to protect your business from claims related to advice, recommendations, or professional services.

No, General Liability Insurance does not cover vehicle-related incidents. You need Commercial Auto Insurance for protection in case of accidents involving business vehicles.

Typically, no. General Liability policies usually do not cover punitive damages, which are fines imposed by the court to punish intentional misconduct.

Intentional acts, such as an employee purposely damaging a client’s property, are not covered by General Liability Insurance. These are excluded because they are not accidental.

No, poor workmanship or faulty work is not covered. This is referred to as the workmanship or warranty exclusion. For instance, if you use the wrong materials and the work deteriorates, this would not be covered by General Liability Insurance.

Just read and in 30 minutes you will know everything about insurance.