Cheap Roofing Insurance Insurance

Find out how we can save you up to 20% with Roofing Contractors Insurance..

We make sure you protect your business from the unexpected with the best Roofing Contractors Coverage.

Let our experienced agents negotiate the most competitive quotes for you while getting the best Roofing Contractors coverage on the market.

Want a phone quote?

GET A FREE QUOTE WITHIN MINUTES

Pick your State to get started! We’ll compare policies from leading providers and show you the best rate after.

All information given is treated very seriously by us and will never be shared. For more information about how we store and secure your data, please refer to our Privacy Policy.

Want a phone quote?

Who We Are

We’re one of the fastest growing providers of liability coverage on the web, offering insurance quotes of all types for contractors in the USA

Get rates from America’s leading insurance providers with an instant quote from us…

What Is Roofing Contractor Insurance?

Being in the business it is no surprise to you that Roofing is one of the four Most Dangerous Jobs In the Country. These dangers are spelled out specifically in the Electronic Library of Construction Occupational Safety & Health.

This policy covers the financial costs caused by damage your operations cause to a client and/or any passers-by. Roofers understand the danger of the job and usually will do anything within their power to protect those on the ground below from falling equipment or debris.

But accidents happen, and that is part of the reason why roofers insurance exists. But no matter how careful you are, accidents still happen. You and your business need to be protected.

The most common hazards roofers face include falls from height, burns, and electrocutions. It is critical that all roofers are well trained. Further, they should be actively attempting to prevent the risk of accidents at all times.

That is why we make it easy for you to get the affordable roofers insurance you need for your business. We can even get you insurance the same day you contact us.

Article Table of Contents

- What Is Roofing Contractor Insurance?

- What Does Roofing Insurance Cover?

- Roofing Insurance Cost

- Roofing Insurance Rates And Coverage

- What Does Roofing Insurance Cover?

- Get Your Free Roofing Contractor Liability Insurance Quote

- What Types Of Insurance Should A Roofer Contractor Have?

- Statewise Roofing Insurance Information

- What Other Roofing Contractors Had to Say About Getting Their Policy Through Contractors Liability…

- Frequently Asked Questions (FAQ)

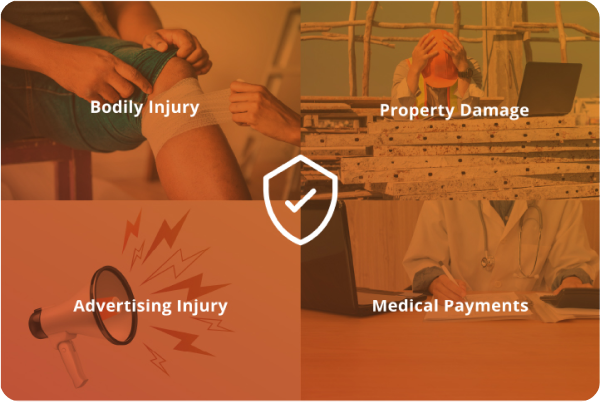

What Does Roofing Insurance Cover?

This policy covers against claims made by their clients and/or third parties for any damage that may have been caused by the contractor or their employees.

Roofing contractors realize that there are risks associated with the work they do and take painstaking measures to ensure safety and their reputation. They usually will go above and beyond to protect their clients and third parties from suffering a loss.

Roofing contractors know that this is how they can differentiate themselves from their competitors and make the business grow. But no matter how vigilant you are, accidents and losses happen. That is the reason why general liability coverage exists.

These are some of the types of damage that are covered under roofers’ general liability policy. There are also some examples of when you might encounter these types of damages:

Injuries to the Body

Any physical harm caused to a third person that you are deemed responsible for.

Example: A piece of unsecured equipment falls off the roof and hits a client or third party in the head, causing a concussion or a broken shoulder.

Advertising Injury

Any false claim or direct attack made against a third party, as in libel or copyright infringement.

Example: You advertise the differences between your company and another roofing company that you specifically mentioned. This results in loss of business on their end and they sue in response.

Damages to the Property

Any damage to the property that is caused by your work.

Example: Piles of roofing debris are left on the lawn of a client for too long, causing the grass underneath it to die.

Medical Payments

Any time a third party sustains a physical or mental injury at your worksite and receives medical attention.

Example: A runner on the sidewalk incurs a broken ankle after tripping on a piece of roofing debris from your project.

Personal Injury

Any non-physical injury that causes harm to the reputation or emotional state of a client or third party.

Example: Provides protection against claims of libel, slander, copyright infringement, invasion of property or privacy, wrongful eviction, false arrest, and similar acts that cause damage to a person’s reputation or rights.

Legal Expenses

This includes attorney fees and any judgments entered against your business. Without coverage, all these expenses will be paid out of your pocket.

Example: This includes attorney fees and any judgments entered against your business. Without coverage, all these expenses will be paid out of your pocket.

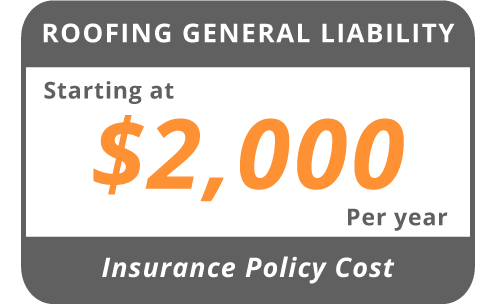

Roofing Insurance Cost

Standard Roofing General Liability Insurance Policies start around $2,000 annually.

However, ContractorsLiability.com recommends that any general costs presented in a quote ought to be thoroughly reviewed, as customized plans will always vary. We want you to feel as though your insurance requirements are being met, so contact us today for a free roofing insurance quote that takes into account your business’s specific needs, as well as more information about your customized insurance plan.

The common factors that insurance companies use to determine roofers insurance costs are:

-

Your company’s accident history

If you’re a company with a clean accident record, then you are less likely to have a high insurance rate than some of your competitors. This, however, does not account for the age of your business, which also plays a role in determining insurance rates.

For example:, A company may have no recorded accidents, but if the company is relatively new, a rate may be higher than an older company with the same record.

-

The average age and legal background of your employees

Employees who do not pass generic background checks, as well as many younger employees, could make your liability insurance higher. A good way to save money if you do hire any of these demographics is to provide consistent and documented training.

-

How old your company is?

If a company has an established history of excellence, an insurance company will see this as a form of reliability, thus encouraging their capacity to offer a lower rate due to lower risk.

-

Where your company is located

Believe it or not, crime can be considered part of a liability package. There is a higher likelihood of property damage due to crime, therefore it is part of the responsibility of the owners to make sure they are covering their assets and reputation.

Roofing Insurance Rates And Coverage

This table displays typical rates and coverage for Roofers General Liability for $1 Million/$2 Million Policy.

| State | Coverage | Next Insurance | Ace Insurance | Rockingham | PCIC | United Specialty | Shield |

|---|---|---|---|---|---|---|---|

| IL | 1M/2M | $3720 | $2910 | $2720 | $2850 | $4110 | $No Coverage |

| IN | 1M/2M | $2850 | $2720 | $4110 | $2990 | $2440 | $2600 |

| CA | 1M/2M | $3110 | $2990 | $3450 | $4110 | $2680 | $2950 |

| PA | 1M/2M | $2440 | $2650 | $2860 | $3070 | $3280 | $3490 |

| NY | 1M/2M | $4220 | $2650 | $No Coverage | $2750 | $2880 | $2750 |

| GA | 1M/2M | $2950 | $3110 | $3410 | $3100 | $2780 | $2990 |

| FL | 1M/2M | $2950 | $3410 | $3880 | $2450 | $2720 | $3100 |

| CO | 1M/2M | $3410 | $2650 | $No Coverage | $2770 | $3410 | $No Coverage |

Annual premium above includes unlimited certificates of insurance.

Rating assumes 150,000 gross revenues for roofing/general contracting with 10% subcontractor costs.

Premium are subject to underwriting approval and financing charges may apply.

Roofers Contractors Insurance Specialized Endorsements

Roofing have specialized needs from other types of contractors. There are specialized endorsements that can cover you for damage caused by weather as a result of open roofs and additional coverage if you use Torch Down Roofing, just to name a few types of specialized General Liability Insurance coverage roofers may want.

So why go for the generic option, which may not account for the coverage you need, when you can get a policy that is specifically designed to protect you? A Tailored policy is the safest and most accurate coverage for roofers contractors, and Contractors Liability can help you find a plan that fits your needs.

Get the right protection for the job!

Instant Free QuoteWhat Does Roofing Insurance Cover?

These are some of the types of damage that are covered under roofers’ general liability policy. There are also some examples of when you might encounter these types of damages:

-

Injuries to the Body:

Any physical harm caused to a third person that you are deemed responsible for.

Example: A piece of unsecured equipment falls off the roof and hits a client or third party in the head, causing a concussion or a broken shoulder.

-

Damages to the Property:

Any damage to the property that is caused by your work.

Example: Piles of roofing debris are left on the lawn of a client for too long, causing the grass underneath it to die.

-

Personal Injury:

Any non-physical injury that causes harm to the reputation or emotional state of a client or third party.

Example: Provides protection against claims of libel, slander, copyright infringement, invasion of property or privacy, wrongful eviction, false arrest, and similar acts that cause damage to a person’s reputation or rights.

-

Advertising Injury:

Any false claim or direct attack made against a third party, as in libel or copyright infringement.

Example: You advertise the differences between your company and another roofing company that you specifically mentioned. This results in loss of business on their end and they sue in response.

-

Medical Payments:

Any time a third party sustains a physical or mental injury at your worksite and receives medical attention.

Example: A runner on the sidewalk incurs a broken ankle after tripping on a piece of roofing debris from your project.

-

Legal Expenses:

This includes attorney fees and any judgments entered against your business. Without coverage, all these expenses will be paid out of your pocket.

It is important to note that roofers’ liability insurance only covers damages to third parties. To cover the medical bills and bodily damage to one of your employees, you will need Workers Compensation insurance.

Get Your Free Roofing Contractor

Liability Insurance Quote

Only 5 minutes of your valuable time.

We can often get same day coverage

What Types Of Insurance Should A Roofer Contractor Have?

Besides General liability insurance Policy for your Roofing Business, there are a number of additional forms of insurance coverage you should consider. The scope and nature of your business will determine which of these policies is best for you. Your roofing company is unique. You have different needs than other roofing companies.

You need to have customized coverages designed for the realities of your business. Just like roofs, no two are alike. They may be similar but each roof has its own peculiarities. Your coverage options need to be based on your needs. This is designed to be a quick summary of the different types of Roofing Insurance coverage you should consider.

-

Business Owners Policy or BOP

This is a bundle of coverages designed for the small roofing business owner. This policy includes property coverage along with liability coverage. Since these coverages are bundled together they are cheaper than if they were purchased separately.

-

Inland Marine insurance/ Tools and equipment insurance

This covers your tools and equipment if they are stolen or destroyed by a covered peril.

-

Professional Liability Insurance/ Errors and Omissions Insurance

If you provide design ideas and recommend different types of roofing solutions you should obtain this coverage. It will cover you in the event advice or recommendations you provide result in a loss to your client. It also will also cover the cost of attorney fees that may be incurred defending you from such claims.

-

Roofing Workers Compensation insurance:

Roofers Workers Compensation insurance protects you and your employees if they become sick or injured in a work-related incident. If you have employees this coverage is required in almost every State. It is also important to remember that you can face Civil Penalties if you have a worker who is injured and you do not have coverage. In some extreme cases, you can even be subject to criminal penalties.

-

Commercial auto insurance:

This covers the vehicle you use in your roofing business. It is important to note that if you are using your personal vehicle for work your personal auto insurance company may deny your claim if you do not have the proper Commercial auto insurance.

-

Product Liability Insurance:

If you sell products in your work, you may want to protect yourself against liability risks. This will provide coverage in the event the product causes a loss to the client.

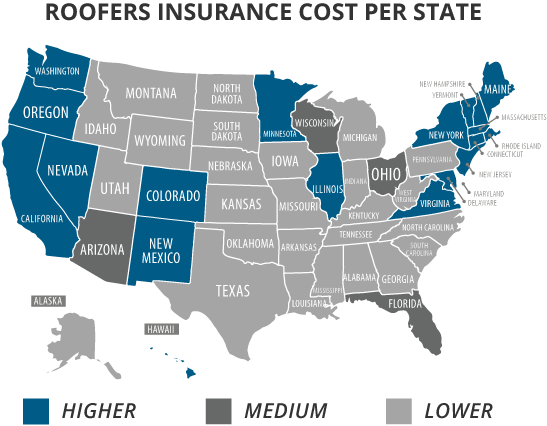

Statewise Roofing Insurance Information

Explore our selection of statewise articles that provide general information on the policies required for roofing contractors in each state. Stay updated and compliant by familiarizing yourself with the diverse insurance requirements and suggestions, ensuring the security and success of your business across different regions.

What Other Roofing Contractors Had to Say About Getting Their Policy Through Contractors Liability…

Contractors Liability made getting roofing insurance a breeze! Their team was knowledgeable and guided me through every step. The rates were competitive, and I felt confident in their coverage. Highly recommend them for any roofing contractor!

– Sarah K.

Contractors Liability provided exceptional service! Their team was very professional and helped me get the perfect insurance coverage for my roofing business. The process was straightforward, and their rates are unbeatable. Highly recommend!

– John D.

Contractors Liability exceeded my expectations. They offered comprehensive roofing insurance at a great price, and their team was incredibly helpful and friendly throughout the process. I feel secure knowing my business is well-protected. Highly recommend them!”

– David M.

I had a fantastic experience with Contractors Liability. They understood my needs as a roofing contractor and provided a tailored insurance plan that fit my budget. Their customer service was top-notch, always ready to answer any questions. Will definitely use them again!

– Mike T

Switching to Contractors Liability for my roofing insurance was the best decision. They offered comprehensive coverage at an affordable price and made the whole process smooth and hassle-free. Their team is professional and friendly. Couldn’t be happier!

– Alex R.

I’m thoroughly impressed with Contractors Liability. They made understanding and purchasing roofing insurance easy. Their customer service was responsive and knowledgeable. The coverage they provided gave me peace of mind. Five stars all the way!

– Emily S

Frequently Asked Questions (FAQ)

The following are common questions about Roofers Insurance.

Roofing insurance is specialized liability insurance that provides custom coverage for accidents that often require coverage legally. Even in states that do not require liability insurance, it is important to consider having roofers’ insurance to protect your company in the instance of an accident.

Unfortunately, no. Roofers’ insurance only covers third parties, like your client or visitors to the worksite. Workers Compensation insurance is what’s responsible for covering your employees. However, this should be no deterrent from purchasing roofers’ insurance, as it can protect your company from serious lawsuits, and in many cases, it is the law to have it. Learn more with our Guide To Workers Compensation Insurance For Roofers.

Roofers’ insurance covers you and your company when punitive damages (penalties against your business), compensatory damages (financial losses), and general damages occur. These are very general terms for a variety of claims that are covered under the umbrella of roofers’ liability insurance.

There are many insurance agencies out there, and you might be tempted to go with the one you see consistently advertised on the television or even one that is closer to home. However, Contractors Liability is certain that if you want the best policy, you need to work with specialized agents like ours. Along with our customer satisfaction guarantee, we:

- Work with A-rated insurance companies, like the large ones advertised in popular media, to get you service that you can trust.

- Customer service iconProvide you with customer service, tailored to your needs from a licensed insurance agent.

- customized policies iconCreate a customized roofers’ insurance plan that fits with your business demographic, history, and future.

- lowest pricce icon Provide you with the lowest price for the best coverage out of any of our competitors.

E-Book Now Available

Learn the nuts and bolts of Contractors Insurance and how to protect your staff, your business and you.

READ NOW

Other Insurance Worth Considering

Builders Risk Insurance

Having builder’s risk insurance shows your clients that you are committed to taking care of their property and are covered for any potential losses.

Commercial Auto Insurance

Keep your business rolling smoothly with commercial auto insurance, covering damages and liability on the vehicles that drive your success.

Tools & Equipment Insurance

Your tools and equipment are the backbone of your business. Insure them with tools and equipment insurance to avoid setbacks and financial hardship.

Workers Compensation

Workers compensation insurance is essential for safeguarding your team from the unexpected. Show your employees they’re valued by securing a policy that protects them on and off the job.