Commercial Or Business Umbrella Insurance

Every business owner should consider commercial umbrella liability insurance. We live in a litigious society. No matter how careful you are, there is always the possibility your business will be sued.

But every small business is vulnerable to a major catastrophe or a lawsuit. Think about some of the devastating losses you have heard about recently and the large settlements that are awarded in courts these days. It is possible these losses could exceed your primary insurance coverage.

Get Fast Quote

Add details for the fastest quote

Call Us 24/7

We’ll answer at any time, call us.

Customer Service (888) 766-4991

What Is Commercial Umbrella Insurance?

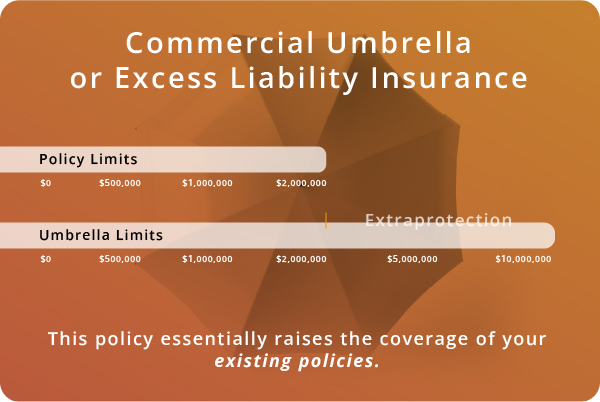

Commercial umbrella insurance is an additional insurance policy commonly bought to maximize coverage terms and limits of another policy.

In addition to your Liability policies, commercial umbrella insurance provides an extra layer of protection if a claim surpasses your liability insurance coverage. This policy essentially raises the coverage of your existing policies.

Anyone with high-value assets or working on a high-risk project should consider a commercial umbrella insurance policy. This may include heavy operating equipment, expensive automobiles, or if you are working on an expensive project for a client.

Commercial Umbrella Insurance is also known as business umbrella insurance or excess liability insurance.

Get An Instant Commercial Umbrella Insurance Quote

You can fill out the online quote form below to get an instant quote or call (866) 225-1950 to talk to an agent now.

How Much Does Commercial Umbrella Insurance Cost?

Umbrella liability insurance is important because it covers these unforeseen events. It is not expensive, and, in certain instances, it could literally save your business. Umbrella coverage is no longer a luxury. With a Contractors Liability umbrella policy, you can get up to $10 million of liability protection over and above the limits of other insurance policies, you have for your business.

Contractors Liability will write umbrella coverage for business liability, Commercial auto liability, and workers’ compensation. The cost of this peace of mind insurance is surprisingly small.

Protect your business. It is competitive, fast, and convenient. If you have any questions while filling out the online application, please call the toll-free numbers displayed or click on the on-line chat button and a licensed Contractors Liability insurance agent will assist you.

What Does Commercial Umbrella Insurance Cover?

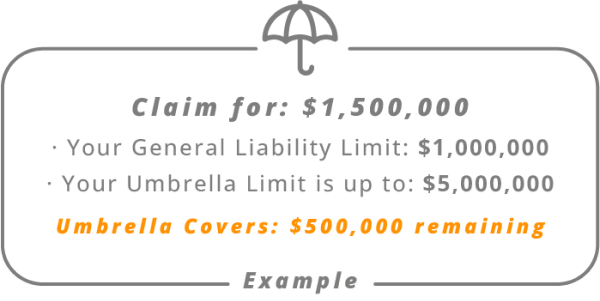

Commercial umbrella insurance provides coverage for the same claims as to your Liability insurance, however, it is used to cover the costs that your policy cannot cover. It does not broaden what is covered, but how much coverage you can get for a claim.

For example:

If your liability policy covers up to $1 million in coverage, but your claim is $1.5 million in damages, an umbrella insurance policy would prevent you from paying the remainder out of pocket.

Reputation Matters

Our customers trust us for great customer service and cost-effective coverage.

Frequently Asked Questions (FAQ)

The following are common questions about Commercial Umbrella Insurance.

Every small business is vulnerable to a major catastrophe or a lawsuit. Think about some of the devastating losses you have heard about recently and the large settlements that are awarded in courts these days.

It is possible these losses could exceed your primary insurance coverage. The possibilities are endless; a plumber might repair a simple pipe and cause a flood, ruining expensive and sensitive manufacturing equipment.

- Policies are crafted to meet your needs

- We negotiate with insurers to achieve effective solutions

- Knowledgeable and professional sales team

- A-rated insurance companies

- 24-hour claims service

- Easy payment options

- Online quotes

- Attention to detail and exceptional customer service

E-Book Now Available

Learn the nuts and bolts of Contractors Insurance and how to protect your staff, your business and you.

Read NowContractorsLiability.com is here to help with all your insurance coverage needs, including specialized plans and tailored insurance policies. All our highly trained agents can help you in English or Spanish.

At Contractors Liability we value and respect your privacy. That’s why we don’t sell or share your information with any third parties and we only use it for our commercial purposes.